Compound Interest and How It Can Help or Hurt You

You’ve probably heard people talk about compound interest since you were in high school. Remember the A = P(1 + r/n)^nt formula you had to memorize for your 9th grade algebra class?

That’s because compound interest is a powerful tool that can either really help or really hurt you and your personal finances.

So… what is compound interest?

In a nutshell, compound interest is when accumulated interest is added to the principal balance... or when interest is added on top of interest.

When interest is lumped into our principal balance, we can start to see an exponential increase in the balance overall.

Pin this post for later!

How does Compound Interest Work?

Let’s back up to our high school math class by quickly reviewing the compound interest formula:

A = P(1 + r/n)^nt

A = Final Amount

P = Principal Balance

r = Interest Rate

n = Number of times interest is compounded

t = Number of time periods total

The most important factors that contribute to compounding interest are principal balance, interest rate, and time.

Now, I’m not saying you need to manually calculate this for each of your accounts. Investor.gov has a great compound interest calculator.

But it’s important to see the formula and understand how compound interest works.

If you really want to do the calculations by hand and need some extra review, check out this great post by Investopedia.

Latest Posts:

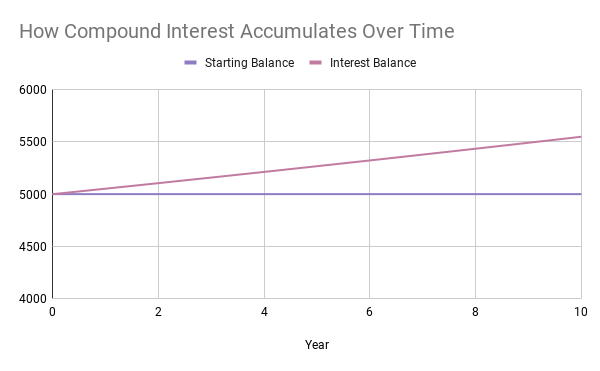

How Compound Interest Can Help You

Let’s say that we put $5,000 into a high yield savings account that is compounded annually for 10 years with a 1.05% interest rate.

If we make absolutely no other contributions to the account, we will have $5550.50 after 10 years because of compounding interest.

The higher the principal balance, the higher the interest rate and the longer the period of time, the more money that will be accumulated.

That’s pretty cool!

The sooner you start saving money and the more you contribute, the more money you will have in the long run.

That’s why personal finance experts recommend individuals start saving for retirement as early as possible, so that they can take advantage of compounding interest.

How Compound Interest Can Hurt You

If you have a debt balance with a high interest rate, compound interest is working against you.

Let’s say you have a $3,500 credit card balance with a 19% APR.

Your credit card balance will accumulate $55.42 in interest each period!!

If you make a $75 monthly payment towards this balance, only $19.58 of that will be applied to your principal balance.

At this rate, it would take you 86 payments… or 7.2 years… to pay off your balance, and you would have paid a total of $2,911.07 in interest.

Yikes.

This is why so many financial experts recommend the Debt Avalanche Method as a debt repayment strategy.

The Debt Avalanche prioritizes paying off debts in the order of highest interest, which makes the most mathematical sense. If you pay off debts with the highest interest rates first, you will likely save more money on interest in the long run.

Closing Thoughts

Compound interest can help us build wealth faster or stay in debt longer.

Understanding the effects of compounding interest is so important when it comes to managing your personal finances. The better you understand it, the better you can use it to your advantage!

If you found this information helpful, please share it on social media using the links below!